READ THE FULL 2022 GREATER OKLAHOMA CITY OUTLOOK.

Oklahoma City’s personal income grew by 3.6% in 2020 even as much of the metro economy remained in a safer-at-home posture. Despite the lack of labor earnings, pandemic relief policy provided income flows sufficient to push income higher. Successive rounds of policy moved personal income up 8.6% in 2021 to $81.5 billion. Direct income support will subside in 2022 but labor market strength and wage inflation will continue to move nominal personal income higher. The baseline expectation is for growth of 5.7% in 2022 followed by much slower growth in 2023 as general economic conditions weaken.

Personal current transfer receipts are government payments to households through programs like Social Security, Medicare, and veteran services. During recessions transfer receipts include items such as direct stimulus payments, extended or expanded tax credit refunds, and federal supplements to unemployment insurance. Many transfer receipts are tied to a measure of inflation. As a result, during non-recessionary periods, transfer receipts grow with population and prices. Over the 2012 to 2018 period, transfer receipts grew at an average annual rate of 2.1%. Transfer payments exploded during the pandemic sending more than $15.6 billion to Oklahoma City metro households through these programs alone, equivalent to $18,194 for every full and part-time worker in the state. Transfer receipts are expected to reset in 2022 but at a higher level because the inflation currently in the system is passed through to these benefits.

Given the tremendous income support provided through transfer payments, it should not be a surprise to find per capita personal income growth through this period. Metro area per capita increase grew to $56,609 in 2021 and will surpass $59,000 in 2023 if current policies can navigate the difficult path ahead. Perhaps more significant is the growth in the Oklahoma City population. After slowing in the middle of the last decade population growth rates have picked up in recent years. Growth is expected to accelerate over the outlook period at 1.5% in 2022 and 1.7% in 2023. A previous discussion highlighted the growing gap between Oklahoma City and the rest of the state. To emphasize that point, note that population growth rates in Oklahoma City were, on average, 2.5 times faster than the growth of the statewide population. The gap in growth rates is accentuated during periods of recession as Oklahoma City is more resilient to economic distress than the rural areas of the state.

The year ahead promises to be defined by the year behind. Strong fundamentals in population and job growth will combine with the residual strength of household balance sheets for a strong start to the year in the labor market. Nonfarm employment is projected to grow at a 4.1% pace in the metro area in 2022. The risks are to the downside but do not reflect concerns for general economic weakness. Rather the downside risk stems from concerns that there is sufficient labor supply to meet this demand. Employment growth slows in 2023 with the downside risk to the outlook now reflecting concerns of general and widespread economic weakness.

The discussion below highlights just a few sectors of the Oklahoma City metro area economy with a full sector forecast available in the appendix tables. It is worth noting the strength expected in some of the region’s larger employment industries in 2022 with health services up 4.8%, leisure services up 6.7%, professional and business services up 6.5%, and financial services up 5.0%. Note that employment spread, especially at the start of the year, is expected to be widespread. How deep into the year this strength can hold remains to be seen and the ensuing slowdown from a shift in policy should also be felt broadly across sectors.

While the unprecedented direct policy support for household income of 2021 is not expected to repeat in 2022, the underlying economic fundamentals are hardly distressed. In-migration and household formation will support local house prices while strong demand for labor will continue to provide earnings opportunities. Households continue to work through existing savings and nearly every layer of government – state, municipal, county, tribal, school district – continues to allocate relief funds accumulated during the previous year. In short, even as both fiscal and monetary policy change course in 2022, an immediate recession is unlikely. The baseline expectation calls for strong private job growth in Oklahoma City in 2022 at 4.0%, as the metro area recovers to pre-pandemic levels of payroll employment sooner than the rest of the state. Conditions will moderate in 2023 with private payroll growth of only 1.7% with any policy misstep or overreach bringing asymmetric downside risk.

Services employment contracted sharply in 2020. For perspective, note that during the 2016 energy recession growth rates in services employment slowed to near 1% in both 2016 and 2017 but remained in positive territory throughout. The aggressive contraction in 2020 is a direct reflection of a pandemic response that discouraged group consumption of services like travel, eating out, and recreation. Those hardest hit sectors posted job gains in 2021 but at an insufficient rate to fully recover to pre-pandemic levels. The baseline expectation is for the recovery to carry well into 2022 with the services sector growing at a 4.0% pace in 2022 before moderating to 2.0% growth in 2023.

Oklahoma City’s oil and gas sector continues to exert a significant economic influence even as direct employment falls with each boom-and-bust cycle. The energy sector’s economic reach reflects long-established supply chains which create significant economic multipliers from local exploration and production activity. As technology advances, however, the direct activity becomes less labor-intensive. Thus, with every energy cycle, employment struggles to regain its previous peak. Current oil and natural gas prices combined with structural forces (like a lack of investment in new production and the inability of renewable energy sources to quickly meet the demand of a recovering global economy) offer upside hope for the sector. Shale production seems poised to rebound in 2022 and while productivity gains have been concentrated in the Permian Basin, projected commodity prices will support a broader-based recovery in 2022. Oklahoma City oil and gas employment is expected to add back jobs over the outlook period to 11,600 in 2023 but will remain far below the 2018 employment footprint of 21,600.

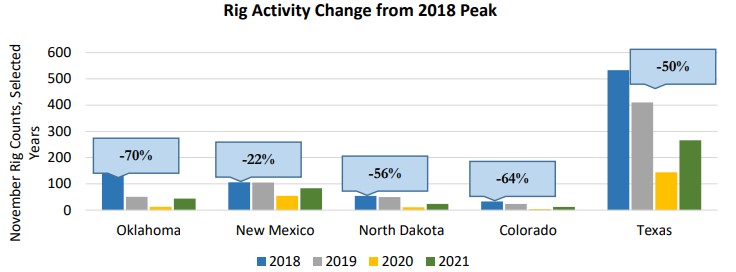

It should be noted that Oklahoma’s oil and gas sector has contracted more sharply and earlier in the cycle than its peers. Rig activity fell abruptly in 2019 long before and unrelated to the pandemic. The pandemic induced recession and withdrawal of a demand for energy drove a further collapse. It makes some sense then that Oklahoma, as the first state to see a drawdown in drilling activity, would be among the last states to experience the recovery. Relative to the 2018 peak, a comparison of drilling activity across years show Oklahoma rig counts are still down 70%. This compares to New Mexico where 2021 rig counts are only down 22% from 2018 (and production has fully recovered) and North Dakota and Texas, each down 56% and 50% respectively. Absent deliberate policy support, Oklahoma’s oil recovery is likely to lag relative to peer states.

The Oklahoma City metro’s economic identity is more complex than that of a simple energy center. With every energy cycle, the city’s identity becomes a little more nuanced. Among the industries that have both a substantive history and a promising future is the city’s aerospace complex. Like the oil and gas industry, aerospace is not easily captured by a single industry. It spans categories from transportation to technical services and from manufacturing to the public sector. A previous independent survey of the broader Greater Oklahoma City aerospace sector revealed more than 43,000 employed across 291 establishments. Tinker Air Force Base remains the largest single site employer in both the state and metro with more than 26,000 employed. The transportation, warehouse, and utilities sector is a good proxy for the industry as it captures much of the maintenance and repair operations. This sector has grown aggressively from 17,800 jobs in 2012 to 31,900 jobs projected in 2023. After slowing to a 5.1% pace in 2021, industry growth will pick up modestly in 2022 before slowing again in 2023 with the expected economic moderation. In the long run though, expect the aerospace complex to be an increasingly important piece of the area’s economic identity.

The Oklahoma City metro should expect a strong start to 2022. In addition to recovering some jobs in the energy sector and sustaining growth in aerospace, the metro area is likely to add jobs in business services, retail trade, health services, and financial services among others. The limiting factor to payroll job growth may indeed be the limited willingness of individuals to engage the labor market as they did before the pandemic. And long-run forces remain favorable as flows to the I-35 corridor and urbanization in the state favor the continued assertion of Oklahoma City as the state’s economic leader. But in the medium term, challenges lie on the horizon. Economic activity will respond to the withdrawal of fiscal support and monetary policy adjustments to contain inflation. The difficulty is in assessing how far away on the horizon these challenges lie. Almost certainly economic activity holds strong through the spring before moderating through summer. A serious economic disruption, should it materialize, would be expected later in 2022 and as we move into 2023. This means that the uncertainty surrounding the 2022 outlook is unlikely to abate ahead of next year’s effort.